Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

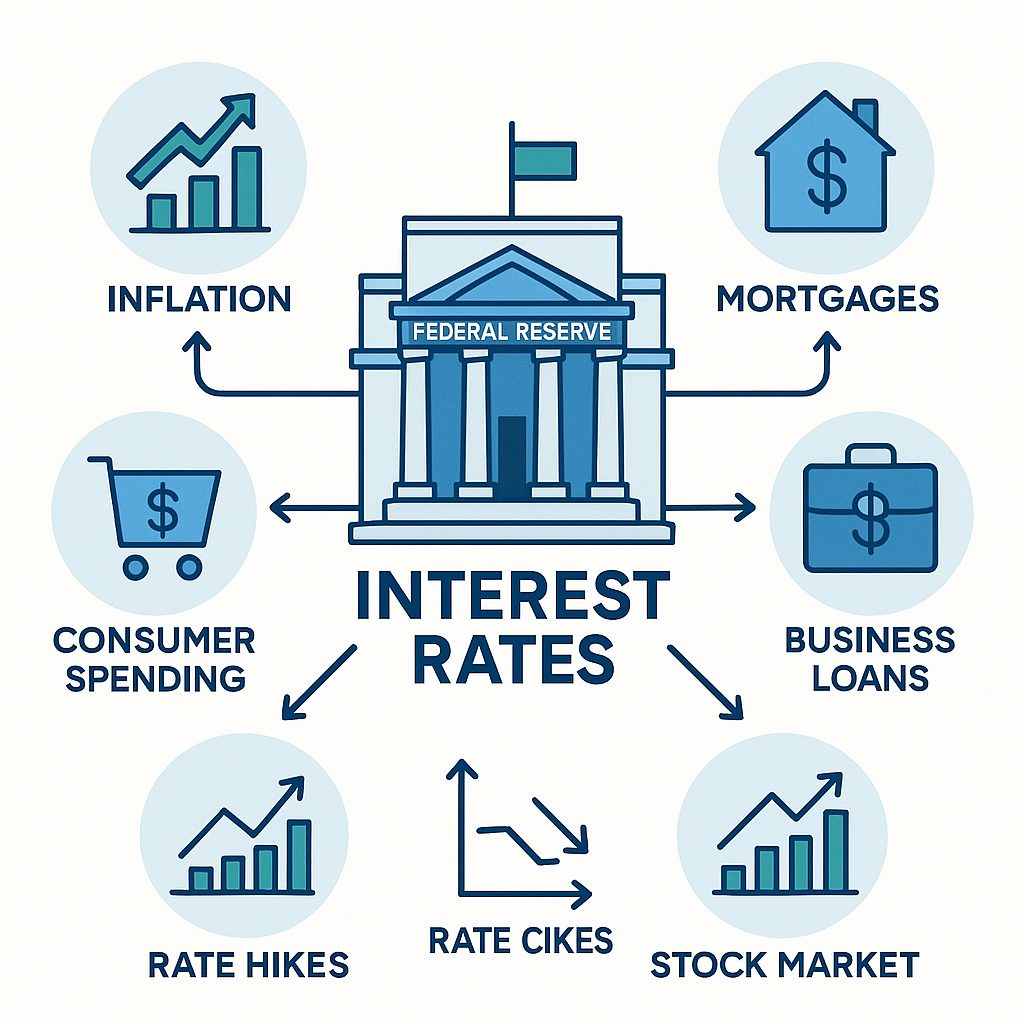

When the U.S. Federal Reserve (the Fed) lowers interest rates, it usually gives the real estate market a boost by as it stimulates the consumer spending, including home buyers previously waiting for rates to come down, and also incentivizes investors. With more rate cuts expected to continue in 2026, homes will be a bit more affordable and buyer activity will likely pick up. However, research shows that there is still a shortage of homes for sale in high-demand areas and prices continue to be inflated.

Impact of Interest Rates Cuts on Home Loans and Buying Power

- Loans: The Fed’s rate cuts mostly affect short-term loans, such as construction loans for builders and home equity lines of credit (HELOCs). For long-term loans, however, the effect is slower and less direct as rate cuts do not necessarily dictate 30-year fixed mortgage rates, which tend to track the 10-year Treasury yield more closely. Nonetheless, national statistics reveal that the average 30-year fixed rate has dropped to approximately 6.22% (mid-December 2025), down from 6.7% a year ago.

- Monthly Payments: The small drop in rates means lower monthly payments for homebuyers. This makes purchasing a home a little more achievable.

- Increased Demand & Affordability: As rates come down, more buyers enter the market, and more homeowners refinance their loans for better terms. Even small decreases in interest rates can open the door to thousands of potential buyers, and homeowners needing to refinance, previously standing by.

Home Supply and Price Dynamics

- Housing Inventory Shortage and Reduced Resale Listings: The real estate market remains constrained by limited supply, largely due to lower new construction in states and counties with strict zoning and construction rules and the “lock-in effect”, which is when existing homeowners hesitate to sell because they would lose their low fixed-rate mortgages (below 4%) for new loans at higher rates.

- High Prices: Despite slight declines in some areas, national prices remain elevated, driven by inflation, and continued strong demand and tight supply. Lower rates could increase competition and push prices up.

- Incentives for Builders: Cheaper short-term borrowing benefits builders, encouraging new construction that may ease supply shortages and help stabilize prices over time.

Outlook and Planning Ahead

Experts claim that low interest rates alone will not solve the housing shortage or high prices. In 2026, analysts expect slow improvement—home loan rates may average between 6.25% and 5.75%, and home sales should rise, but results will vary by location. In any event, each case is unique, and you should not be intimidated by the state of the market and the Fed’s decisions on interest rates.

If you are looking to buy or invest, explore resources available to you and discuss affordability with at least three different reputable lenders to learn more about your options and future possibilities. Being informed and planning ahead will always be in your favor. Additionally, many home sellers and new-construction builders are offering rate-buy down as incentives for buyers. On the flip side, if you are a homeowner looking to sell, consider a pricing strategy that plays in your favor and is comparable to today’s fair market prices, avoid over pricing your home and consider offering incentives that appeal to buyers to make the purchasing of the home more affordable.